Biden Calls on Fed to Continue Digital Dollar Research

Digital photography killed the Polaroid. The mp3 rendered the CD obsolete. When was the last time you sent a postcard rather than snapping an Instagram-worthy selfie? Analog has taken a beating from digital over the past few decades, and that competitive mismatch may be coming for the wrinkled, faded bills in your wallet.

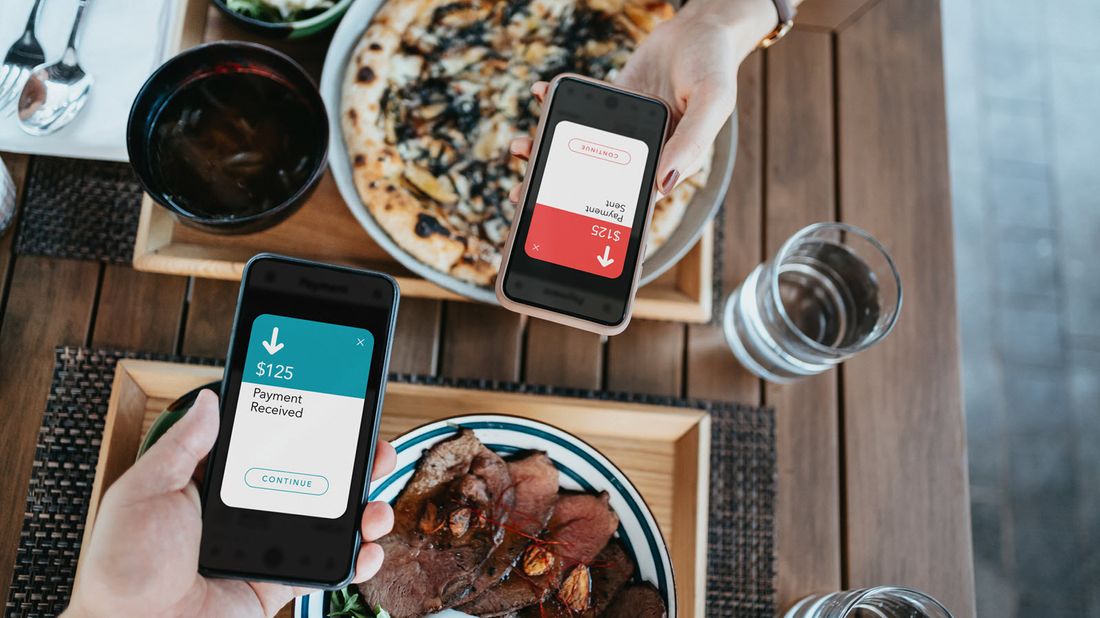

According to McKinsey, 78 percent of Americans used a digital payment method in 2020, whether it was sending a P2P payment, shopping online, in-app purchases or using a contactless, digital payment method in store. More and more commerce is conducted in 1s and 0s rather than Washingtons and Lincolns, and that’s caught the attention of the White House, Federal Reserve and other central banks around the world.

Earlier this month, President Joe Biden signed an executive order directing federal agencies to evaluate the risks digital assets may pose to the U.S. economy and financial system. Ultimately, the order sets the stage for future cryptocurrency regulation by the U.S. government.

Meanwhile, as digital payments penetrate deeper into modern economies, the Fed is thinking about taking the shift to digital a step further by establishing a so-called central bank digital currency (CBDC), or digital dollar that’s fully backed by the United States. In fact, Biden’s order specifically places urgency on government CBDC research and encourages the Fed to continue existing efforts. But what exactly is a digital dollar, and why is the Fed considering it?

What is a digital dollar?

Money in the U.S. comes in two forms: physical cash and reserves held by financial institutions with the Fed. A digital dollar would represent a third version of money that uses digitally tokenized “dollars” (essentially a unique identifier) to instantly settle transactions between people, businesses and across borders. A master ledger, or single source of truth (governed centrally by the Fed or in a more distributed, rules-based model like a blockchain network), would track the history of every single transaction and verify the unique ID of each digital dollar to ensure legitimacy and instantly transfer funds from wallet to wallet. Just like the dollar, the supply of digital dollars would be controlled and backed by the Federal Reserve.

A digital dollar would represent a big step change in the U.S. financial system’s plumbing, but you probably wouldn’t notice much from a user perspective. We can already send money “instantly” to a friend via Venmo or pay a bill online with a credit card. It sure feels like digital money, but all these “instant” services are financial sleight of hand. While the business or friend you paid “receives” the money immediately, behind the scenes, the fintech or credit card company is making a short-term loan to pay your friend or the business while the transaction is settled. That settlement process between your bank, your credit card or Venmo account, your friend’s app and their connected bank takes time to reconcile. This is our current system, and it’s known as an account-based system of money.

A digital dollar would boil that entire process down to a single step because transactions would be settled directly on the Fed’s balance sheet via the token-based digital ledger system – no intermediaries needed other than a digital wallet app. In this system, when you send your friend a “digital dollar,” it lands directly in their digital wallet, and its authenticity and history of transfer is verified and recorded against the Fed’s centralized digital ledger. Done.

An innovation platform

Efficient policymaking: Because a digital dollar would be issued and managed entirely by the Fed, it could expedite monetary policy implementation. For example, your digital dollars could earn interest simply sitting in your wallet (rather than on a bank’s balance sheet). The interest rate could vary daily or change based on rules or policy goals of the Fed. Emergency stimulus, for example, could be sent directly to wallets from the Fed in a very targeted, instantaneous fashion.

Efficient transactions for consumers and businesses: Because there isn’t a settlement process, a digital dollar would make paying friends, businesses and suppliers easier. Money could move around the world instantly and without a chain of intermediaries in between. That would save time and reduce transaction costs.

Tokenization: Because each digital dollar’s unique identifier and location would be tracked in a distributed ledger that’s constantly synchronized, it becomes near impossible to make a counterfeit. It’s also easier to track fraud and make secure transactions, given there’s a single source of truth that tracks who has paid what to whom and when.

Conditionality: This will likely become a digital currency buzzword. This simply means a digital dollar can be “programmed” with rules for use. For example, an insurance company could program digital dollars to automatically land in a farmer’s account when monthly rainfall dips below a specified threshold. Parents could send digital dollars to their college-age child but programmatically limit its use so it could be spent only in the bookstore and not on beer.

Financial stability: A digital dollar would essentially remove all risk of a bank run or other liquidity risks that can arise due to the lag in settlement periods. That’s because all the transactions are occurring directly on the Fed’s balance sheet rather than on a bank balance sheet that’s then reconciled with the Fed’s. Though many of these risks have been greatly reduced over time, a retail CBDC effectively renders this structural issue obsolete.

Improved economic data and forecasting: It would be easier to aggregate transaction data and gain insight into how money is spent, where and why. This could improve policy and provide highly accurate, real-time economic data for financial services firms and investors.

Why is the Federal Reserve researching a digital dollar?

International competition is rising. The U.S. dollar is the standard currency in the global financial world; however, central banks around the world are exploring digital currencies. While it would take some time, digital currencies from other countries could put competitive pressures on the U.S. dollar’s position as a global standard currency, particularly if they create operational efficiencies for businesses and consumers. China, for example, is already experimenting with a digital currency, and a host of other countries are eyeing their own.

It’s the Fed’s job. The Federal Reserve, like other central banks, is designed to carry out four major functions: provide the unit of account for the monetary system, ensure finality of payments using its balance sheet, ensure the monetary system functions smoothly, and maintain the integrity and competitiveness of its monetary system.

If consumer trends are shifting and a digital dollar could yield efficiencies and economic competitiveness, the Fed, by its own mandate, should at the very least explore how such a system might work. The dollar’s dominance in world finance yields clear advantages for the U.S., particularly as it pertains to borrowing and servicing its debt. The Fed will want to maintain this advantage.

Disruption from cryptocurrency. Crypto allows instant transactions and settlement, but there’s very little oversight from a government or regulatory authority. To some that’s the whole point. However, that means there are no consumer protections, guarantees or assurances backed with the full faith of the U.S. government behind a single crypto. A digital dollar could reduce such risks while offering the same technological capabilities.

“You wouldn’t need stablecoins; you wouldn’t need cryptocurrencies if you had a digital U.S. currency,” Fed Chairman Jerome Powell said recently. “I think that’s one of the stronger arguments in its favor.”

Potential disadvantages

Privacy concerns: Who maintains the ledger? How much information is tracked with each transaction? Can users be identified, or will their identities be encrypted? Will the Fed manage the central ledger, or will it be distributed like the blockchain? These are key questions to grapple with, as privacy and data tracking could run up against Constitutional concerns.

Destroy established business models: A digital dollar could render certain financial services obsolete if adopted on a wider scale. Or, it could compress profit margins enough that it becomes difficult to compete. If your digital dollar earns interest, do you need to “store” it at a bank anymore?

Even with wide-scale adoption, the Fed probably won’t be interested in handling day-to-day functions like customer service, tech support and app development. While the transactions will settle with the Fed, banks, fintechs and companies that have yet to be founded will likely be needed to offer wallet apps, new services based on a digital dollar and more.

Accessibility: Not everyone has a smartphone or easy access to an internet connection. A digital dollar will require a device and connectivity, which could exclude disadvantaged groups from participation. To be fair, a digital dollar will likely operate alongside physical currency for decades to come, but inclusivity will be a hot topic as digital currency discussions evolve.

Cybersecurity risk: Lastly, while a token-based ledger system infrastructure is, by design, more secure, no system is infallible. What’s more, digital wallet apps wouldn’t be immune from the same phishing, malware and other hacking techniques that exist today.

The Fed's progress on research

To date, no decision has been made on whether to issue a digital dollar in the U.S. However, given the dollar’s important position globally, the Fed is deep in research and exploring policy development paths. In addition to research underway at the Federal Reserve Bank of Boston, the Fed is also working with the Bank for International Settlements’ CBDC coalition and private sector companies involved in the space.

While we’re still far from widespread adoption of a digital dollar, expect the conversation to grow rather quickly over the next few years.

Protect your most valuable asset.

Your income helps fund your financial plan. Your advisor can show you how to help protect that income so your plan stays on track.

Find your financial advisor